AFR Banque Palatine 2025

-

-

Statement by the person responsible

I hereby certify that the information contained in this annual financial report is, to the best of my knowledge, true and accurate and contains no omission liable to impair its significance.

I declare that, to the best of my knowledge, the annual financial statements and consolidated financial statements were prepared in accordance with the body of applicable accounting standards and that they provide a faithful presentation of the assets, financial position and income of the company and all the companies included in the consolidation, and that the management report appearing on page 4 presents an accurate picture of the development and income of the company and the financial position of the company and all the companies included in the consolidation, as well as a description of the main risks and uncertainties to which they are exposed, and that it was prepared in accordance with applicable sustainability reporting standards.

-

1Board of Directors’ management report

Economic environment

2025 was characterised by moderate global economic growth, reflecting an international context still marked by trade tensions and political uncertainty. According to the International Monetary Fund’s January 2026 World Economic Outlook, global gross domestic product growth is expected to be around 3.3% in 2025, stable compared with 2024 but higher than previously forecast thanks to the resilience of some major economies. This momentum is accompanied by significant regional disparities, while risks related to protectionism and persistent imbalances weigh on the outlook.

In 2025, the US economy is expected to grow moderately but at a much slower pace compared to previous years, with a GDP growth projection of around 2% (2.1% according to the World Bank report published in January 2026). The slowdown is linked to political uncertainty, trade tensions and weaker domestic demand. This expansion, well below the historical trend, reflects a context in which investment and consumption are gradually decreasing.

On the labour market, the unemployment rate is forecast to be around 4.4%, up slightly from a year earlier, a sign of a gradual tightening of the job market.

At the same time, inflation remains a significant challenge, with persistent pressures fuelled by tariff hikes and import costs, which could keep price developments well above the 2% target if these effects are increasingly transferred to the economy. The consumer price index therefore stood at 2.7% in December across the Atlantic.

Activity indicators published throughout the year show contrasting trends: while the ISM (Institute for Supply Management) services index remained above the expansion threshold overall (below the 50-point level), signalling continued growth in the services sector, that of the manufacturing sector was often below 50, indicating a contraction or stagnation in the US industrial sector.

For their part, confidence indicators showed a downward trend reflecting continued caution among business leaders and increased consumer concern about the economic outlook and price developments. These combined signals of activity and confidence illustrate the structural challenges facing the US economy, with companies hesitant to invest more and households increasingly sceptical about the future evolution of the labour market and purchasing power.

Within the Eurozone, growth continued at a moderate pace, with Gross Domestic Product (GDP) estimated to expand by nearly 1.3% according to Eurostat data, reflecting a slow but resilient recovery driven by domestic demand, while exports remain constrained by an uncertain global context. Spain’s economic momentum is noteworthy, as the country was driving European growth with GDP up 2.6% this year.

The unemployment rate remained at a relatively low level of 6.2% in December, showing a gradual improvement in the labour market despite national disparities.

Inflation has continued to decline, approaching the European Central Bank’s target of around 2%, although pressures on service prices remain persistent. Inflation in this area stood at 3.4% in December, compared with 1.9% for the overall index.

Emerging and developing economies continue to outperform advanced economies, despite a marked global context of persistent trade tensions. India remains the main driver, with GDP growth estimated at 7.2% according to the World Bank, supported by strong domestic demand, controlled inflation and significant structural resilience. China, however, is growing at a more moderate level close to 4.9%, reflecting the challenges of its structural transition from an export-oriented and industrial economy to a service- and consumption-oriented economy, as well as an ageing workforce that is weighing on growth potential. The country also has to deal with high corporate debt and tensions in the real estate sector, while also facing trade and technology tensions with the United States and the European Union, factors that are holding back some foreign investment and exports.

Against this backdrop, the world’s main stock markets experienced an eventful but generally positive year in 2025, marked by all-time highs and periods of extreme volatility.

The CAC 40 and EuroStoxx 50 have often reached or come close to record levels, driven by solid results from European companies as well as investor appetite despite macroeconomic uncertainties. The flagship index of the Paris stock market gained just over 10%, and the main European equity index rose 18.3% to 5,791 points.

In the United States, the major indices also ended the year with strong growth, with double-digit gains for the S&P 500, the Dow Jones and the Nasdaq, boosted in particular by enthusiasm around artificial intelligence (AI) and hopes of rate cuts by the US Federal Reserve (Fed).

On the commodities market, the year was marked by a notable divergence – precious metals such as gold and silver exploded to record levels driven by safe-haven demand and institutional buying, while oil suffered from a supply surplus and weaker demand, leading to significant price drops for crude. Gold has had a record year, with the price of an ounce rising to more than $4,300 at the end of the year, up nearly 65%. As for a barrel of oil, prices were down nearly 20% this year, to around $60.

Finally, cryptocurrencies experienced high volatility, with a significant bull phase pushing the “queen” of cryptocurrencies, Bitcoin, to an all-time high of around $125,000 in October, before being adjusted at the end of the year to finish at around $88,000.

Interest rate trends

The European Central Bank continued to normalise its monetary policy, with inflation expected to stabilise around the 2% target in the medium term. After four 25-basis-point cuts in the first half of the year, the ECB stabilised its key interest rates in the second half of the year while reaffirming an economic data-dependent approach. Therefore, the deposit rate, the refinancing rate and the marginal lending rate are set at 2.00%, 2.15% and 2.40% respectively. At the same time, the asset purchase programme (APP) and the pandemic emergency purchase programme (PEPP) continued to decline in a measured manner, as the ECB was no longer reinvesting the principal payments of maturing securities.

In 2025, the Fed adjusted its monetary policy gradually to keep pace with inflation and the labour market. After maintaining the target range for the federal funds rate in the range of 4.25%–4.50% for much of the year, the Federal Open Market Committee (FOMC) opted for a gradual reduction in rates at the end of the year, lowering the range to 3.50%–3.75% to support activity in the face of a moderate economic slowdown and inflation still above the 2% target, but on a downward track. The Fed continued to moderate the pace of balance sheet reduction, while remaining attentive to risks to jobs and prices, reflecting a cautious approach aimed at balancing its dual mandate. Internal monetary policy developments have also been marked by dissent over the scale and timing of adjustments, reflecting debates about the need for more severe tightening or more significant easing depending on incoming economic data.

Global interest rates continued to reflect both monetary policy developments and sovereign market dynamics.

In the Eurozone, the €STR short-term interbank rate stood at 1.92% at the end of the year, down by almost 100 basis points compared to the start of the year, reflecting the impact of the ECB’s decisions. The 3-month Euribor was around 2%.

Longer-term interest rates showed a different trend, as measured by swap rates, which at 2 years rose by just over 5 basis points to 2.2% and at 10 years by just over 50 basis points to 2.9%.

Yields on 10-year Eurozone sovereign bonds also rose, particularly given the growing financing needs for some countries. In France, bonds were also sensitive to political and budgetary uncertainty. The OAT ended the year at 3.6%.

In the United States, interest rate momentum was generally downward, both on monetary rates and on the 10-year US Treasury financing rate. Despite pressure on the dollar at the end of the year, the Secured Overnight Funding Rate (SOFR) fell by just over 60 bps to 3.9%. As in the Eurozone, the US swap yield curve steepened by around 50 basis points due to the more marked decline in the 2-year rate than that observed in the 10-year rate. Finally, on the bond market, the yield on US 10-year debt fell to 4.2% at the end of the year.

Outlook for 2026

Current global growth projections for 2026 show a broadly stable profile. However, this scenario remains surrounded by many uncertainties: the evolution of trade tensions (lull or resurgence), impact on the increasing integration and growing use of artificial intelligence, as well as geopolitical risks.

On this last point, the joint military operation carried out by the US and Israeli armies in Iran since the end of February could have significant repercussions, depending on its duration and a possible desire by the Iranian leaders to regionalise the conflict.

-

2Palatine sustainability report

Part 1 - General Information

1.1Basis for preparation

1.1.1BP 1 - General basis for the preparation of sustainability statements

Palatine prepared its sustainability report in accordance with the sustainability reporting standards adopted under Article 29b of Directive 2013/34 of the European Parliament and of the Council of December 14, 2022 (European Sustainability Reporting Standards or ESRS). These standards provide a comprehensive framework for the disclosure of non-financial information on environmental, social and governance issues.

The bank's sustainability report is based on a double materiality analysis, which takes into account both Banque Palatine's impact on the environment and society, and the impact of environmental and social issues on the company's performance. This approach ensures that the sustainability report is relevant to all stakeholders, including employees, investors, clients and the communities in which the Bank operates. It results in a list of impacts caused by the Bank's activity, and of risks and opportunities (IRO) related to environmental and societal changes.

To prepare this report, Palatine has collected data on a consolidated basis and across its value chain. This sustainability report is audited as required by the regulations with a limited level of assurance.

Scope of the sustainability report

The scope of consolidation used for the sustainability report is the same as for the financial statements.

The following subsidiaries are included in Palatine's consolidation and are exempt from the obligation to provide individual and consolidated sustainability information: Palatine Asset Management and Ariès.

Any exclusions from the reporting scope by family of indicators are mentioned in the description of each indicator or in footnotes where applicable.

Option to omit specific disclosures

Palatine has not made use of the option that allows it to omit certain disclosures relating to intellectual property, know-how or the results of innovations. This option is provided for in Section 7.7 of ESRS 1: Classified and sensitive information, and information on intellectual property, know-how or results of innovation.

Nor has Palatine made use of the exemption from reporting disclosures on imminent developments or deals under negotiation, in accordance with Articles 19a(3) and 29a(3) of Directive 2013/34/EU.

1.1.2BP 2 - Disclosures in relation to specific circumstances

1.1.2.1Time horizons

In most cases, the material impacts, risks and opportunities have been assessed in the short, medium and long term. To obtain this forward-looking information about Palatine in the sustainability statements, the general principles as defined in Section 6.4 of ESRS 1 section were used:

- •1 year as short term (annual financial statement presentation period);

- •Between 1 year and 5 years as medium term;

- •More than 5 years as long term.

When the time horizons deviate from these general guidelines, this information is communicated at the same time as the relevant information concerning the specific material subject. During the preparation of this sustainability report, forward-looking estimates and assumptions were made. The results observed may differ from these estimates and assumptions.

1.1.2.2Value chain estimates

The indicators must cover the entire consolidated scope. However, for the calculation of greenhouse gas emissions under ESRS E1-6 (greenhouse gas emissions), the indicator is calculated over an extended scope. Scope 3, category 15 emissions relate to the value chain, in particular financed emissions.

In order to calculate Scope 3 category 15 emissions on the banking book, greenhouse gas data come from several sources:

- •purchase of supplier data (Carbone4, Trucost, CDP);

- •data collected from Palatine clients (EPD - Energy Performance Diagnostic); and

- •public databases (Centre Scientifique et Technique du Bâtiment and ADEME).

When data is not available, Groupe BPCE, which performed the calculation for all the entities within its scope concerned by the sustainability report, including Palatine, uses sector-specific intensity estimates: extrapolation or PCAF proxy.

1.1.2.3Sources of uncertainty concerning estimates and outcome

This report, known as the "Palatine sustainability report", was prepared in accordance with the legal and regulatory requirements resulting from the transposition of the European Directive on the disclosure of information on companies' sustainability (Corporate Sustainability Reporting Directive or “CSRD Directive”). This second year of application is characterised by uncertainties about the interpretation of the texts, which are generalist and cover all sectors of activity but do not specify a specific framework for banking and financial business models. There is also the absence of established practices or comparative information and certain data, in particular within the “value chain”.

With regard to what follows, Palatine has drawn on all the work done by Groupe BPCE in preparing its own sustainability report.

Groupe BPCE has endeavoured to apply the normative requirements set by the ESRS, as applicable at the date of the sustainability statement, based on the information available within the timeframe for its preparation, by doing its best to reflect its role as a universal bank-insurer, as well as its various business models.

For the double materiality analysis and, in particular, that relating to its value chain, Groupe BPCE encountered limitations relating to the maturity of its valuation methodologies and the availability of data. As presented in section 1.4.2 - List of material IRO, on the Environment (E) topic, Groupe BPCE considered that only the issue of mitigation and adaptation related to climate change is material within the meaning of the standard. The limitations relating to the market information and methodologies available at this stage did not make it possible to characterize the Nature ESRS’s materiality within the standard’s meaning, which led the Group to assess these environmental issues as non-material. This assessment was carried out based on the definitions of the standard, and the methodologies available to assess and carry out the rating exercises. This assessment can be explained, in particular, by the absence of a consensus on robust methodologies developed on the topics in question and of relevant and appropriate data which would make it possible to establish a link between the impact or risks for Groupe BPCE regarding these topics through its value chain. In view of Groupe BPCE’s continuous improvement approach to these environmental issues, the work and ongoing changes in international methodologies, the standards that are being put in place, the best market practices that are emerging and information and data from its customers, which should gradually become available, this double materiality analysis may change in the coming years. The dual materiality analysis, the results of which are presented in this report, aims to qualify the impacts, risks and opportunities as described in the CSRD standard: this analysis only meets the needs of sustainability reporting and not the analysis of factors risks presented in the chapter on risk management.

For the data points presented in this report, Groupe BPCE used methodological options that it deemed relevant and estimates for numerous data, particularly concerning the various activities in its value chain. The data, analyses, and studies carried out do not guarantee that expectations and targets will be achieved: they are based on objectives, commitments, estimates, assumptions, standards, and methodologies under development and currently available data, which continue to evolve and develop. Some of the information in this document was obtained from public sources, sources that seem reliable, or market references: Groupe BPCE has not verified it independently. In addition, Groupe BPCE notes that the information expected in terms of sustainability is based on so-called “agnostic” European standards (ESRS), which are generalist and do not reflect the specificities of the financial sector. As a result, certain data items deemed irrelevant or not applicable, given Groupe BPCE’s business models and value chain, have not been produced. The same applies to certain data points relating to the taxonomy regulation.

Regarding the climate change mitigation and adaptation transition plan, in its transition plan, Groupe BPCE distinguishes between actions relating to its own operations and the targets and actions that it has set itself in order to contribute to the decarbonisation of the economy by supporting its clients. The actions described present, in particular, the achievements and roadmap for the actions that seem to impact the downstream value chain. The Group’s transition plan describes past, current and future efforts to align its financing, investment and insurance portfolios with scientifically established trajectories aimed at achieving global carbon neutrality by supporting its customers with their environmental transition. This report does not quantify the effects of decarbonisation levers or future estimates of total financed emissions. Indeed, the actions undertaken by the Group cannot replace those of individual clients, companies or States that it supports with the transition, and the transition of the economy to a low-carbon economy depends on many parameters external to Groupe BPCE.

Regarding the assessment of greenhouse gas emissions, as a service company, the Group emits a limited level of CO2eq in terms of its own operations, including by integrating the upstream value chain (purchases, including those related to IT and technological investments, mobility including business trips, etc.) and its clients travelling to its branches or business centres. Regarding its assessment of greenhouse gas emissions, in addition to its own operational emissions, the Group takes into account an estimate of the emissions associated with certain activities in its upstream and downstream value chain, including in particular its investments. In this respect, a significant proportion of the emissions recorded come from so-called "financed" emissions, measured according to a standardised method applicable to category 15 of the GHG Protocol, based on the allocation to the institution of a share of the issues of financed or held counterparties. It is estimated that financed emissions can, on average, account for three times the same greenhouse gas emissions for portfolios exposed to companies in the same value chain. For this sustainability statement, the Group considered the mandatory categories of financial assets provided for in the Greenhouse Gas (GHG) protocol for calculating financed emissions. The scopes, methodologies used and the main assumptions and data sources are detailed in the paragraph relating to (E1-6) “Gross Scopes 1, 2, 3 and Total GHG emissions”.

With regard to Taxonomy, the assumptions used and limitations are detailed in chapter 2.1 Indicators of the European taxonomy on sustainable activities.

Groupe BPCE believes that the expectations reflected in these forward-looking statements are reasonable; however, they are subject to numerous risks and uncertainties, are difficult to predict, generally outside of the control of Groupe BPCE, sometimes unknown, and may lead to results or cause events to unfold significantly differently from those expressed, implied, or anticipated by the aforementioned information and forward-looking statements.

1.1.2.4Changes in the preparation or presentation of sustainability information

No material change in the definition or calculation of metrics, including those used to set targets and monitor progress towards their achievement.

1.1.2.5Reporting of errors in prior periods

1.1.2.6Publication of information from other legislation or widely accepted sustainability information frameworks

Palatine has defined sustainability risk as a risk factor in its risk management framework. The chapter on environmental, social and governance risks under Pillar 3 ESG describes how the Bank defines and manages these risks. This chapter also contains an overview of the impact of climate and environmental risks on other types of risks. Further details on the methodologies and management used for traditional types of risks, such as credit risk, market risk, operational risk and liquidity risk, are provided in chapter 4 - Risk Management.

In addition, the elements relating to the eligibility and alignment of the Bank's portfolios as defined in Regulation (EU) 2020/852 and supplemented by Delegated Regulations (EU) 2021/2178, 2021/2139 and 2023/2486 are included in chapter 2.1. Indicators of the European taxonomy on sustainable activities.

1.1.2.7Incorporation of information by reference

In order to avoid duplication, ESRS 1 allows the incorporation of parts prepared in other documents, such as the management report or the Universal Registration Document, by means of a simple mention, provided that this information has equivalent characteristics, particularly in terms of reliability. This generally concerns the parts relating to the description of the company’s activities and strategy, its governance, remuneration policies, risk factors and the duty of care. The ESRS consider that it is essential to ensure and explain consistency between the sustainability report and the financial statements, paying particular attention to significant amounts, assumptions and projections. Amounts considered material from the financial statements must be accompanied by a reference. While the presentation of a reconciliation in the form of a comparative table between the amounts of the sustainability report and those of the financial statements remains optional.

Requirement Name

Publication

Data point

Registration Document

Document Section

Reference

Disclosures in relation to specific circumstances

ESRS BP-2 Para. 15

Annual report

Chapter 4 – Risk Management Report

The role of the administrative and management bodies

ESRS 2 GOV-1 Para. 19 & 21

Annual report

Chapter 1.3 – Report on corporate governance

Risk management and internal controls over sustainability reporting

ESRS 2 GOV-5 Para. 36 (a)

Annual report

Chapter 4 – Risk Management Report

1.2Strategy

1.2.1SBM-1 - Strategy, business model and value chain

1.2.1.1Sustainability strategy

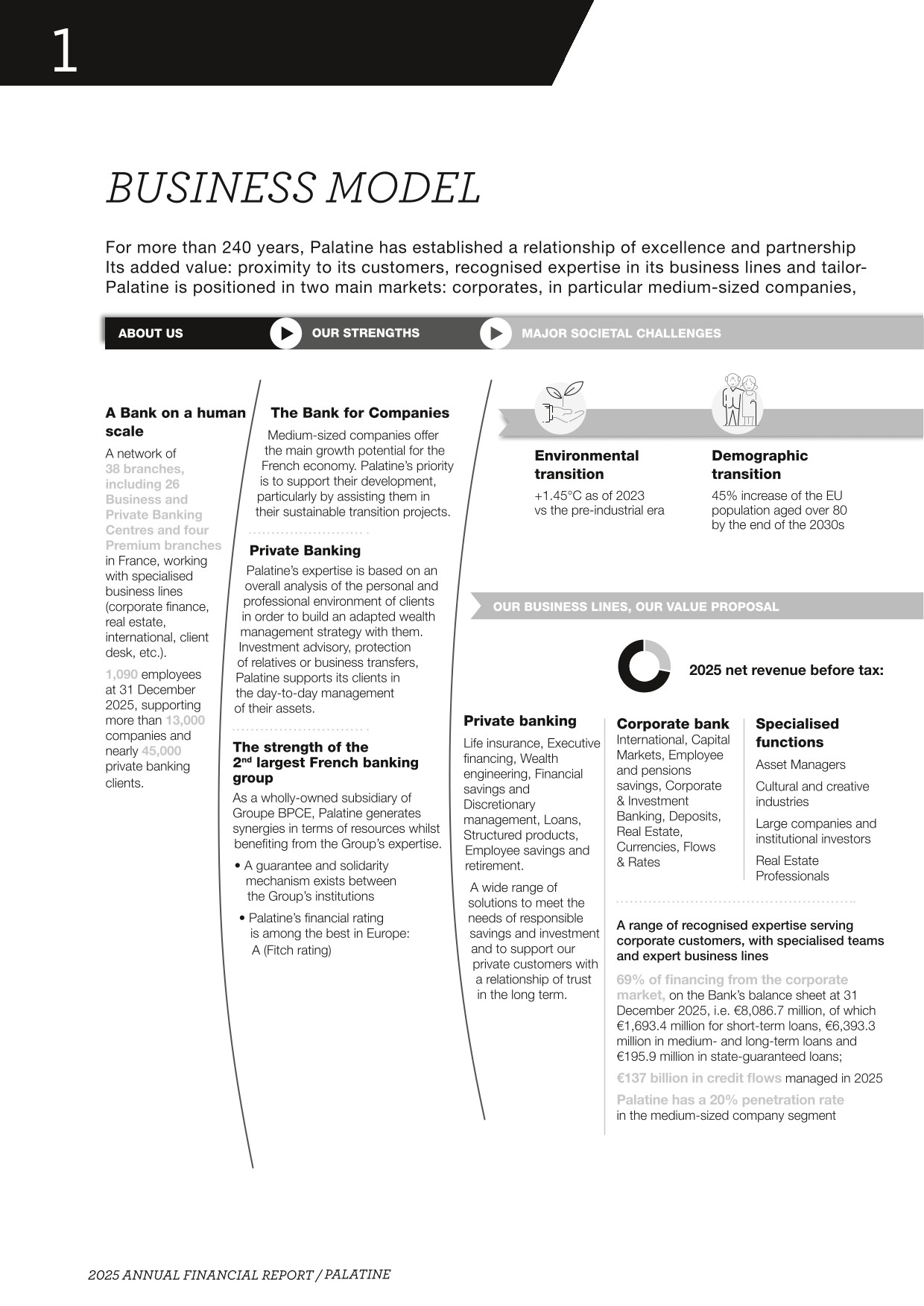

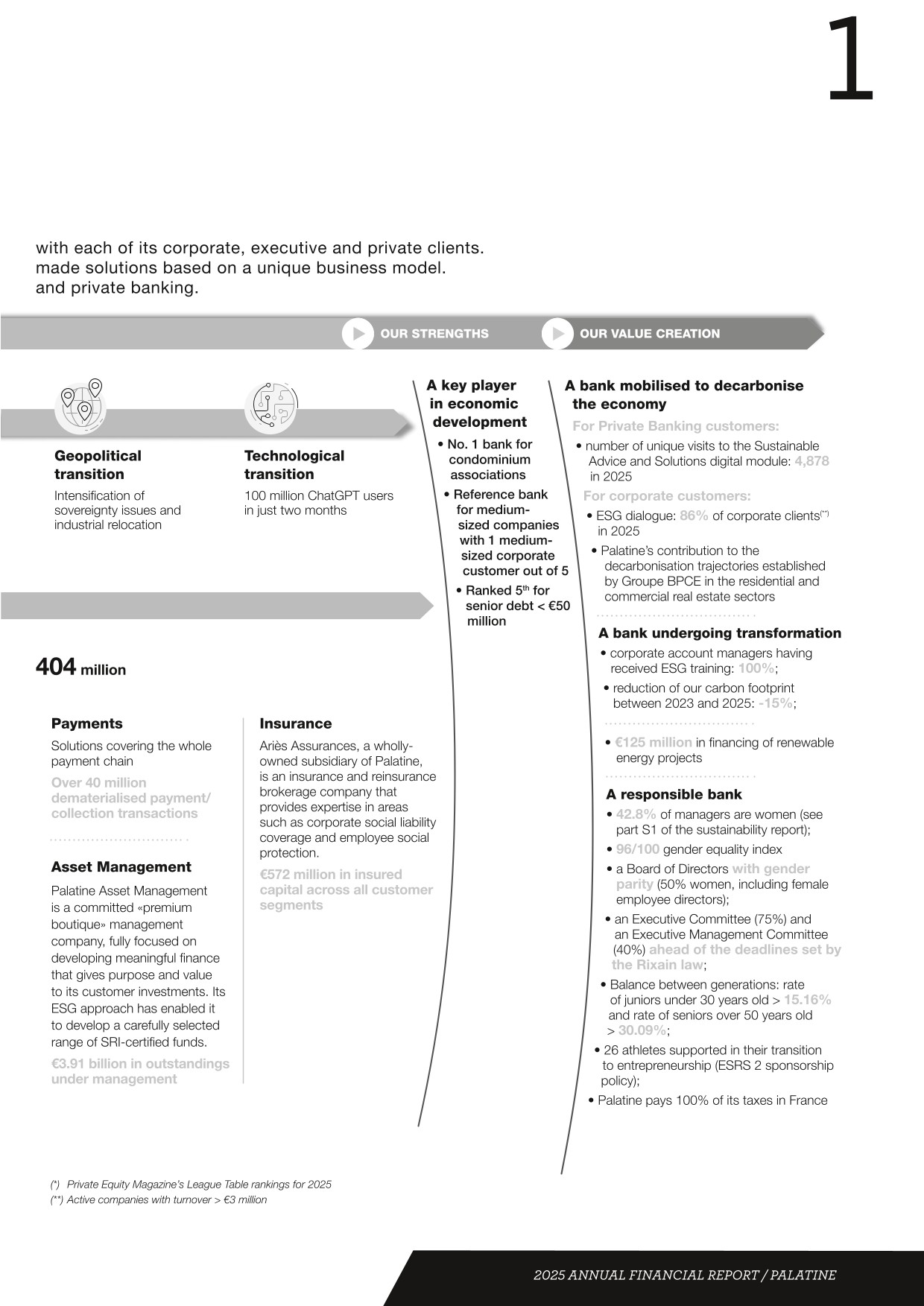

Palatine is part of Groupe BPCE, the second largest banking group in France. A little more than 1,000 employees serving 13,000 corporate clients and more than 45,000 private clients work closely with natural persons or legal entities, responding in a concrete way to the needs of the real economy.

In 2025, faced with environmental, demographic, technological and geopolitical challenges, Palatine was fully committed to financing French medium-sized companies and supporting all its clients in adapting to their new environment.

At the same time, Palatine has been attentive to the working conditions of its employees. Efforts focused on career support, mobility, skills development and recruitment.

On the environmental aspect, in addition to the continuation of awareness-raising workshops on climate issues for the Bank’s employees, the Sustainable Finance Programme has continued, with the aim of better addressing clients’ needs for support and transition-related services.

Faithful to its commitment to community involvement and its values, Palatine continued its societal actions, made donations and supported charitable projects (see section 1.2.3 Sponsorship policy – partnerships).

Characterised by gender-balanced governance, promoting gender equality is therefore a key focus of its strategy.

Palatine therefore intends to continue all its projects aimed at promoting greater integration of environmental and social issues into its activities and relations with its stakeholders between now and 2030. This will notably involve continuing to provide special support to its medium-sized corporate clients and senior executives committed to sustainable, low-carbon and carbon-neutral growth, and including three separate projects with clearly defined objectives in its new Palatine 2030 strategic plan.

Palatine 2030

In 2025, the roll-out of the Palatine 2030 strategic plan, defined in 2024, continued. It is based on a purpose co-built with the Bank’s employees, where Palatine demonstrates its desire to actively engage in order to contribute to the energy and environmental transition by reducing its carbon footprint and supporting its clients in improving their impact.

The purpose of the Bank is thus defined: “As a banking house since 1780, we have been shaping our know-how, our agility and a culture of excellence to be the trusted partner of our clients, both Corporate and Private Banking. We are convinced that French medium-sized companies and their senior executives are at the heart of the economic and socio-environmental challenges of today and tomorrow. As entrepreneurs at the service of entrepreneurs, we contribute to a more sustainable economy by investing in the success of their development, transformation and transmission projects”.

Clients are placed at the centre of Palatine’s strategy as a fundamental priority. Risk expertise is confirmed as a marker of its differentiation. Finally, people are at the heart of its focus, making it the bank where the future of work is being shaped and experienced every day.

Palatine's 2030 vision is broken down into 7 structuring focuses, which reflect the priorities of its development plan in terms of innovation, excellence and performance:

- •the bank of 1 in 4 medium-sized companies and 1 in 2 family-owned medium-sized companies,

- •the reference bank for supporting medium-sized companies in their transitions,

- •the benchmark for senior executives in terms of Private Banking,

- •the leading bank for asset managers (ADB),

- •a bank that innovates to strengthen its businesses in the areas of risk, data and new technologies,

- •a bank with the “Great place to work” label,

- •in the top 3 banks in the cultural and creative industry (cinema, streaming platforms, e-sports structures, content creators, live entertainment, etc.).

Among the major cross-functional projects launched in late 2024 to achieve the ambitious targets set for 2030, one was an overarching project aimed at taking the "Engagé RSE" label to the next level. The objectives were to: minimise the Bank's direct footprint, increase its positive impact on relevant environmental and societal issues, and strengthen its engagement with all its stakeholders. This was implemented by obtaining the "Engagé RSE" label at the "confirmed" level in December 2025. Another structuring project centred on sustainable finance, with objectives including training sales teams in sustainable finance, a programme that has already been completed for corporate account managers and will continue for private bankers in 2026, defining and implementing the Bank's green strategy, setting up a Palatine hub, leading a community of sustainable finance experts, and expanding its offering.

Environmental impact

Faced with the climate emergency, Groupe BPCE and Palatine's approach aims to rapidly implement and deploy measures to mitigate and adapt to the already tangible environmental and socio-economic impacts of climate change and the erosion of biodiversity. Making impact accessible to all means raising awareness and massively supporting all its customers in the environmental transition through expertise, consulting offers and global solutions.

By drawing on science-based scenarios, Groupe BPCE and Palatine are positioning themselves as facilitators of transition efforts, with a clear and ambitious objective: to align their financing and insurance portfolios with trajectories based on scientific scenarios compatible with the objectives of the Paris Agreement.

- •Impact solutions

- •for Private Banking customers: support energy renovation by offering financing solutions and by mobilising its role as an operator, trusted third party as well as its partnerships:

- −by offering a "Sustainable Advice and Solutions" tool in partnership with ADEME, enabling people to easily calculate their carbon footprint and receive advice and assistance for energy renovation work, carbon-free mobility or green savings,

- −by supporting energy renovation projects for condominiums at each stage: energy assessment, search for subsidies, completion of work guarantee, with pathways and financing adapted to each situation,

- −by increasing the number of financing for the energy renovation of buildings,

- −by offering sustainable solutions for investor clients with a range of responsible savings and investments: sustainable development passbook savings accounts, funds with a sustainable investment objective, themed-labelled funds, etc.

- •for corporate customers: supporting the transition of its medium-sized corporate customers’ business models. Palatine is committed to engaging in dedicated dialogue and providing sector-specific expertise to integrate ESG issues according to their size and economic sector, particularly in energy and transport infrastructure, etc.;

- •for Private Banking customers: support energy renovation by offering financing solutions and by mobilising its role as an operator, trusted third party as well as its partnerships:

- •a support for the evolution of the energy mix: faced with the climate emergency, the priority is to accelerate the transition to a sustainable energy system:

- •by playing a leading role in the financing of debt projects for the renewable energy sector,

- •by increasing its financing dedicated to the production and storage of green electricity,

- •by providing financial support and advice through specialist partners to assist the energy transition of medium-sized companies, particularly in the industrial sector,

- •by supporting the reindustrialisation of regions and energy sovereignty,

- •by leveraging dedicated teams of experts in both project financing and business transition support;

- •alignment of its financing, investment and insurance portfolios with trajectories compatible with the objectives of the Paris Agreement:

- •by developing systems to measure carbon emissions,

- •by developing its system for identifying and managing climate, physical and transition risks to which its clients and its own activities are exposed, in a spirit of continuous improvement,

- •by gradually withdrawing from activities with the highest emissions, in particular through adapted ESG policies.

Societal impact

Palatine is committed to supporting local and national initiatives and assists organisations in the fields of art and culture, gender equality, sport.

1.2.1.2Sustainability targets

Among the strategic priorities of its new VISION 2030 strategy, Groupe BPCE is renewing its commitment to environmental and societal transitions. It is committed to making the impact accessible to all and to strengthening its global "positive impact" through the strength of its local solutions.

Sustainable Finance indicators

Achieved 2025

2026 target

HQLA ESG (1)

25.5%

25%

Production of renewable energy

Green portion of Palatine financing production

29% of total corporate financing production in 2025

25% of total corporate financing production in 2026(2)

Production impact loans

ESG questionnaire (active companies turnover > €3 million)

86%

100%

- (1)HQLAs are assets that can be quickly converted into cash without significant loss of value. They are used by banks to meet liquidity requirements, such as those imposed by the short-term liquidity ratio (LCR) under Basel III. ESG HQLA are compliant with Environmental, Social and Governance (ESG) criteria.

- (2)Due to the changing geopolitical context and European regulations.

1.2.1.3Business model

Palatine, a hybrid business model within Groupe BPCE

1.2.1.4Description of major product groups, markets and/or client groups targeted

Palatine, a wholly-owned subsidiary of BPCE SA, serves approximately 58,000 clients in France: 13,000 corporate clients and 45,000 Private Banking clients. Mainly dedicated to mid-sized companies, senior executives and Private Banking, it has been supporting entrepreneurs both professionally and personally for more than 240 years. It provides them with a range of banking products (current accounts, real estate and personal loans, financial investments, financing solutions to meet environmental challenges) and insurance products. Its network consists of 38 branches, including 26 business and Private Banking centres and 4 premium branches.

Palatine offers value-added expertise dedicated to supporting its clients’ growth and performance: wealth, legal and tax engineering, investment advice, global approach to senior executives’ assets, corporate finance, specialised approach to real estate, trade finance, client desk, etc.

In the regulated real estate market, where the bank is the market leader, and in the audiovisual market, where it is a key player, it deploys a dedicated national organisation.

Its slogan “The art of being a banker” illustrates Palatine’s desire to develop a local relational model based on excellent support for its clients.

Palatine Asset Management, a wholly-owned subsidiary of Palatine, is a “premium boutique” asset management company focused on developing useful finance that gives meaning and value to its client's investments.

Its value proposition is focused on the search for sustainable investment solutions to meet different investor profiles from institutional to private customers.

Its team, comprising around thirty employees with complementary profiles, has solid expertise in fixed income management, equity management and diversified management. This expertise is reflected in its range of funds and its portfolio management offer.

1.2.1.5Description of products and services prohibited in certain markets

ESG policies govern the activities of Groupe BPCE in sectors considered sensitive from an environmental, social and governance (ESG) point of view, including those of Palatine.

In addition, Palatine has established strict rules regarding financing for real estate professionals: if the financing concerns an older residential property with an Energy Performance Certificate (EPC) rating of E, F or G, it can only be granted if renovation investments are planned. The same applies to commercial assets of less than 1,000 m² that do not meet the minimum criteria defined by the bank.

Palatine Asset Management activities

As part of its Responsible Investment approach, Palatine AM was quick to implement a policy to exclude the coal sector and monitor contentious issues in order to reduce its exposure to ESG risks, as well as its policy of excluding controversial weapons.

By excluding these issuers, Palatine AM wishes to focus its investment choices on the most responsible companies.

These exclusion lists have since been expanded to include the tobacco, oil and gas sectors, companies that violate the principles of the United Nations Global Compact, non-transparent issuers and, finally, the most carbon-intensive electricity producers.

In parallel with this exclusion policy, Palatine AM is also committed to engaging with companies to encourage them to improve their environmental, social and governance practices. The objective is to promote long-term sustainable performance.

The full policy is available at the following address: Palatine AM exclusion policy

1.2.1.6Labels and commitments

Public commitments that meet demanding international standards

Groupe BPCE and Palatine have made several long-standing commitments to scale up their actions and accelerate the positive transformations to which they are contributing.

Groupe BPCE

Global Compact

Since 2003, the Group has been a participating member of the Global Compact (United Nations Global Compact), which defines ten principles relating to respect for human rights, labour standards, environmental protection and the fight against corruption.

Principles for responsible banking, UNEP Finance Initiative

Groupe BPCE signed the Principles for Responsible Banking on 23 September 2019 and is committed to strategically aligning its activities with the United Nations Sustainable Development Goals (SDGs) and the Paris Climate Agreement.

Net Zero Banking Alliance

Since 2021, Groupe BPCE has relied on the work of the Net Zero Banking Alliance (NZBA), an initiative of UNEP-FI that established a methodological framework for aligning banking books with the objectives of the Paris Agreement. This science-based methodological framework has already been used by more than 100 banks internationally, enabling unprecedented collective mobilization. This alliance has since changed its articles of association and no longer has any members but retains the reference framework it has built.

Thus, Groupe BPCE has published its positions on the eleven sectors of the economy with the highest carbon emissions (electricity production, oil and gas, automotive, steel, cement, aluminium, aviation, commercial real estate, residential real estate, maritime transport and agriculture).

act4Nature

By joining act4nature international in 2024, Groupe BPCE strengthened its commitment to the environment by renewing the partnership supported by Natixis since 2018.

The act4nature international coalition mobilises businesses, public authorities, scientists and environmental associations to protect, promote and restore biodiversity. By joining it, the Group has set itself 24 ambitious targets as part of its activities as a bank, insurer and investor.

Palatine Asset Management

Principles for Responsible Investment (PRI)

In addition, the principles for responsible investment (PRI) were introduced by the United Nations in 2006. This voluntary commitment, aimed at asset management players, encourages investors to integrate environmental, social and governance (ESG) issues into the management of their portfolios. The PRI are a means for promoting the generalisation of the consideration of non-financial aspects by all financial businesses.

At the end of 2019, Palatine Asset Management joined the signatories of the principles for responsible investment.

Palatine

“Engagé RSE” label

In May 2024, Palatine was awarded the "Engagé RSE" label by AFNOR for the first time, achieving the "progression" level. In December 2025, the Bank strengthened its commitment to CSR by achieving the next level, corresponding to the "Confirmed" status of the "Engagé RSE" label. This label assesses the maturity of an organisation's CSR initiatives based on ISO 26000, a recognised international standard. It also serves as a strategic tool for reflecting on and engaging with CSR-related issues, while promoting internal buy-in, steering and structuring CSR initiatives with stakeholders. This step marks a significant turning point in the Bank's CSR commitment and underlines its role as a player in the climate transition.

Professional Equality Label

Palatine has been awarded the Professional Equality Label by AFNOR. Valid for 4 years, this label is a mark of recognition from an accredited independent body for the actions performed in favour of professional equality.

Cancer@work label

On 11 December 2025, Palatine received the Cancer@Work award, recognising the company's commitment to preventing job loss and supporting the continued employment of people affected by cancer or chronic diseases. Since 2016, the Bank's membership of the Cancer@Work network has reflected its belief in the importance of occupational health. Several actions have been put in place, such as a system for donating days of leave and a digital space dedicated to chronic diseases, facilitating access to resources and promoting awareness. This label illustrates the Bank's desire to support its employees, particularly in times of vulnerability, while drawing inspiration from the best practices of other committed companies.

1.2.1.7Value chain

As a financial institution, Palatine receives funds in the form of deposits or purchases of financial instruments by investors and grants loans to its clients (banking transformation function).

The downstream value chain includes clients who benefit from Palatine's products or services, particularly loans.

1.2.2SBM-2 – Interests and views of stakeholders

It is essential for Palatine to take its stakeholders into account in order to improve how it identifies and assesses its sustainability impact. Palatine’s stakeholder consultation process is based on a number of systems that aims to involve them in its process of identifying and assessing impacts, risks and opportunities, as well as levers for improving both environmental and societal topics. These systems are detailed in the table below.

The expectations of Palatine's stakeholders are also identified and taken into account through regular contact with the senior executives of the Banques Populaires and Caisses d'Epargne, as the board members of Palatine are corporate officers of these institutions. But also via meetings with rating agencies, discussions with regulators, image surveys and prospective surveys. In addition, because of Palatine's desire to establish a quality relationship with its partners, the Bank collects "the voice of suppliers". A survey, rolled out in 2025, assessed suppliers' satisfaction with their working relationship with Palatine. This survey will be repeated in 2026. Listening to clients both in qualitative and quantitative terms is one of the founding principles of the approach which allows Palatine to better understand its clients and provide them with a tailor-made response. The customer listening system was overhauled in 2023 in order to solicit all of its customers to express their level of satisfaction and report any dissatisfaction. On two occasions, as part of the certification of the Bank for its CSR approach by the certification body AFNOR, in February 2024 and December 2025, Palatine called on a number of its stakeholders: whether they were internal (with its employees, members of the SEC; Groupe BPCE) or external (clients, partners, suppliers, high-level sportsmen or women supported by the Bank, associations, board members).

Finally, surveys of the Bank's employees, such as the Ipsos survey conducted in 2025, and regular meetings with staff representatives are all useful ways of identifying changes in stakeholder expectations. All these dialogues fed into Palatine's double materiality analysis.

Stakeholders

Dialogue methods

Purpose and results

Board members

- •Participation in specialised committees

- •Training programmes and seminars

- •Participation in the definition of strategic orientations

- •Monitoring function, in particular risk management and reliability of internal control

Employees

- •IPSOS survey (internal survey measuring Palatine's social climate) and job satisfaction barometer

- •Annual interviews

- •Training

- •Internal communication

- •Non-profit networks (women, intergenerational, LGBT+)

- •Employee whistleblowing rights

- •Consultation of employee representatives and representative trade unions

- •Improving quality of life at work, health and safety at work

- •Employee loyalty and commitment (career and talent management, skills and expertise development)

- •Participation of employee representatives in major strategic and transformation issues and negotiation of agreements

- •Measurement of satisfaction

Customers

- •Interviews

- •Strategic dialog to integrate ESG issues

- •Customer events

- •NPS satisfaction surveys

- •Institutional and commercial partnerships

- •Voting policies (available on the websites of the asset management subsidiaries)

- •Definition of offers and customer support

- •ESG dialogue: customer acculturation on ESG issues, support for transformation initiatives, risk assessment for better prevention and management by the customer and for incorporation of ESG criteria in the granting of loans

- •Improving customer satisfaction

- •Monitoring of the respect for compliance and ethics rules in commercial policies, procedures and sales

- •Complaint management

- •Mediation

Suppliers and sub-contractors

- •Responsible purchasing policy

- •Regular meetings with strategic suppliers

- •“Supplier voices” survey

- •Preparation of certifications

- •Listening system and satisfaction surveys

- •Supplier whistleblowing rights and establishment of an independent mediator

- •Audit

- •Responsible Supplier Relations Charter, involving suppliers in the implementation of duty of care measures

- •Compliance with ESG clauses included in contracts

- •Identification of progress plans to better understand supplier expectations

- •Improving the level of satisfaction and the relationship

- •Consultations and calls for tenders

- •Measurement of satisfaction

Institutions, federations, regulators

- •Regular meetings (public authorities, regulators, chambers of commerce and industry, etc.)

- •Contribution to the work of the financial market, participation in sectoral working groups

- •Responses to public consultations

- •Transmission of information and documents

- •Constructively contributing to public debate and participate in collective, fair and informed decision-making

- •Taking into account sector specificities

- •Regulatory compliance

Rating agencies, investors and independent third parties

- •Regular dialogue, participation in meetings (technical meetings, roadshows, conferences, etc.)

- •Transfer of information and documents for ratings/audits

- •Publication of official documents: annual report, half-year report, press releases, investor website

- •Improving transparency

- •Diversification of the Group’s refinancing, in particular by promoting the issuance of Green/social/sustainable bonds

- •Improving financial and non-financial ratings

- •Meeting the expectations and questions of investors and rating agencies

- •Publication of reports

NGOs and non-profits

- •Calls for projects

- •Sponsorship

- •Employee volunteering, skills sponsorship

- •Regular discussion

- •Contributions to market questionnaires

- •Board seats

- •Positive impacts through numerous cultural and solidarity initiatives in various fields: business creation, integration, solidarity, young people, sport, environmental protection, etc.

- •Improving transparency

- •Contribution of cross-expertise: banking/financial and better understanding of local players

Academic and research sector

- •Relations and partnerships with business schools and universities

- •Participation in forums and events

- •Discussions and consultations with scientific experts

- •Recruitment of work-study students and interns

- •Improving the employer brand

- •Contribution to the Group’s research, working groups and strategies

1.2.3Sponsorship policy - partnerships

Palatine's philanthropic commitment, coordinated by the Corporate Secretary's Office and the communication department, organises its actions around three priority areas: gender equality, sport and culture. In the sports field, Palatine works to promote gender equity and equity between able-bodied and para-athletes through initiatives such as the Palatine Women Project programme, support for athletes via the French Sports Foundation, and sponsorship of the Alice Milliat Foundation. The cultural sector also benefits from Palatine's support through partnerships with regional contemporary art structures (Contemporary Art Museums in Lyon, Bordeaux, Nantes, FRAC Sud in Marseille, Luma in Arles), the Opéra-Comique de Paris, and support for the audiovisual industry via the Gloria Palatine prize.

In addition to these priorities, Palatine supports the fight against cancer through its commitment to Cancer@work and the Institut Gustave Roussy, in particular through its participation in the Odyssea and Movember events, as well as a micro-donation system in 2025 for the benefit of Institut Curie and the Fondation des Femmes.

In 2025, Palatine intensified its environmental commitment by partnering with Planète Urgence for the MOSOTRY mangrove restoration project in Madagascar and by offering a tree to each employee via EcoTree in order to fight against climate change and the erosion of biodiversity. As a premium partner of the Paris 2024 Olympic and Paralympic Games, Palatine continued to support four athletes through the French Sports Foundation's performance pact, selecting a gender-balanced team. The Palatine Women Project programme is now in its fourth year, supporting ten high-level female athletes towards entrepreneurship. The commitment to the Alice Milliat Foundation has taken the form of actions in the field, raising awareness and promoting female athletes, particularly during the Festival des Sportives en Lumière and the Alice Milliat Trophies. Cultural patronage was renewed with several institutions and extended to LUMA Arles in 2025, thus supporting artistic creation and access to culture while developing social and educational initiatives. The collaboration with Série Séries was strengthened by the creation of the Gloria Palatine prize, rewarding the representation of women in the audiovisual industry.

Looking ahead, Palatine intends to continue and expand its commitments, in particular through the Palatine Women Project, including exploring the creation of a dedicated endowment fund, renewing its support for the French Sports Foundation, expanding its cultural patronage with the Centre d'art Caumont, and renewing its commitment to the French Golf Federation. In accordance with its CSR 2030 roadmap, Palatine will develop new partnerships with a positive societal impact, maintain its commitments to the fight against cancer, increase its contribution to biodiversity projects and continue to support the arts and culture.

1.3Governance

1.3.1GOV-1 - The role of the administrative, management and supervisory bodies

This part is described in detail in chapter 1.3 – Corporate Governance Report and in Section GOV-2 below.

1.3.2GOV-2 - Information provided to and sustainability matters addressed by the undertaking’s administrative, management and supervisory bodies

1.3.2.1Sustainability topics addressed by the administrative, management and supervisory bodies

Organisation of governance relating to Palatine’s sustainability matters

Palatine's decision-making bodies incorporate transparency, ethical behaviour, respect for stakeholder interests and the principle of legality. They also take the duty of care regarding CSR actions into account.

The Board of Directors is composed of eight board members (non-executive) and Executive Management is composed of a Chief Executive Officer and a Deputy Chief Executive Officer (both executives). On 31 December 2025, the Board of Directors was composed of four women and four men, including two board members representing employees. This brings the proportion of female board members on the Board of Directors to 50%, including those representing employees.

Sustainability matters come within the remit of two bodies within Palatine: the Corporate Secretary's Office (CSR Department) and the Sustainable Finance Programme. The Secretary General and the Programme Director both report to the Chief Executive Officer or the Deputy Chief Executive Officer and are members of Palatine’s Executive Management Committee, and the Secretary General is invited to attend the Executive Committee.

The Executive Committee validates the ESG strategy, ensures its implementation and oversees risk management (the composition and diversity of the Committees and Board of Directors, and of executive governance, the roles and responsibilities of the bodies are detailed in chapter 1.3 - Corporate Governance).

The Board of Directors meets as often as the company’s interests and legal and regulatory provisions require, and at least once per quarter. Several specialised committees have been set up by the Supervisory Board and carry out their activities under its responsibility. Their duties are defined in the Board of Directors’ internal rules. The Chair of each of these committees reports on the committee’s work to the Board.

Various CSR topics are submitted to the Board of Directors for information and decisions. In particular, in 2025, the following were presented: the 2024 sustainability report published in 2025, the double materiality matrix for the 2025 sustainability report, the progress on drafting the sustainability report, focuses on Palatine's actions relating to biodiversity and philanthropic actions, the outlook and challenges, as well as the calendar of CSR actions, the CSR and sustainable finance projects of the Palatine 2030 strategic plan, presented at a Board of directors' seminar and at a Board meeting, and the CSRD audit plan. The workplace equality policy was also discussed.

- •on a quarterly basis at the Executive Management Committee (comprising around fifteen board members representing the Bank's main business lines) and in particular during the progress review of the Palatine 2030 strategic plan;

- •regularly in the Executive Committee (e.g. approval to engage the bank in a CSR certification process, sponsorship, etc.).

Training of governance relating to Palatine’s sustainability matters

Information concerning sustainability expertise that members of the bodies possess directly or can mobilise is further elaborated in chapter 1.3. - report on corporate governance.

1.3.3GOV-3 - Integration of sustainability-related performance in incentive schemes

Concerning the members of Palatine's Board of Directors

Sustainability performance is not taken into account in the calculation of board members' remuneration, as presented in chapter 1.3 of the corporate governance report.

Concerning the effective managers who are members of executive management

- •A fixed remuneration which primarily reflects professional experience related to the position held and the responsibilities exercised, and is determined by comparison to market practices.

- •Annual variable remuneration, 40% of which is indexed to quantitative criteria (net revenue before tax, COEX and net result, Group share), 20% to criteria linked to BPCE's results and 40% to qualitative criteria, which can amount to, when the targets are met, 80% of the fixed remuneration for the Chief Executive Officer (50% for the Deputy Chief Executive Officer) and up to 100% of this same base amount (62.5% for the Deputy Chief Executive Officer) in the event of outperformance. These criteria are shared by the members of the Executive Committee and the Executive Management Committee.

The award of annual variable remuneration partly depends on the implementation of the bank's CSR goals. In recent years, CSR indicators have been: the professional equality index (5%), the increase in SRI outstandings (10%), the share of impact loans, including green loans, in the production of corporate loans (10%), the employee engagement rate (5%), assessment of the green strategy (5%), the NPS rate (10%), implementation of the CSR and green strategy (10%). They are reviewed annually. Those adopted for 2025 were as follows: CSR and green strategy (10%); NPS rate (10%).

The Board of Directors, through its Remuneration Committee, is responsible for setting the method and amount of remuneration for each effective manager. It ensures that CSR issues are fully integrated into the remuneration policy.

1.3.4GOV-5 - Risk management and internal controls over sustainability reporting

1.3.4.1Main features of the risk management and permanent control system related to the sustainability reporting procedure

Preparation and publication of sustainability information

The development and processing of sustainability information within Palatine is mainly the responsibility of:

- •General Secretariat including the CSR and Financial Communication Department;

- •Sustainable Finance Programme.

The General Secretariat, and more specifically the CSR Department, played a key role in coordinating the work of preparing the CSRD sustainability report:

- •coordination of project committee and governance internally, including interaction with other Group entities that prepare their own sustainability report;

- •operational coordination of the work carried out by all contributing departments;

- •increased coordination of the processes for producing the regulatory indicators required by the ESRS;

- •interaction with auditors.

- •coordinating and producing presentations of annual and half-yearly results, the financial structure to enable third parties to form an opinion on its financial strength, profitability and outlook;

- •coordinating and preparing the presentation of regulated financial information (annual and half-yearly report) filed with the French Financial Markets Authority (AMF).

The effective management of the sustainability report production process

The General Secretariat proposes, validates and implements the ESG strategy with the Sustainable Finance Programme. It plays a cross-functional role, carrying out the following key missions:

- •co-constructs the Palatine 2030 strategic plan for the Impact section on the E, S and G aspect;

- •develops and deploys ESG expertise and ensures that the Group is represented and communicates in the market;

- •conducts and interprets scientific and competitive monitoring and supports regulatory monitoring;

- •ensures overall coordination and supports each business line while implementing the necessary synergies.

- •double materiality analysis: this assessment was managed exclusively by the General Secretariat (for a detailed description, see ESRS 2 IRO-1);

- •the identification of impacts, risks and opportunities (IROs) relevant to the Bank’s activity was coordinated by the Corporate Secretary's Office, drawing on Groupe BPCE's work,

- •assessment of the materiality of these IROs: BPCE's Impact Department has established a methodology for rating IROs for the Group. At Palatine, this rating process was coordinated and supervised by the Corporate Secretary's Office, in liaison with the internal stakeholders mentioned above. The business lines and functional departments are responsible for rating the IROs within their scope;

- •communication strategy and editorial content: the General Secretariat is responsible for the bank's Impact strategy and ensures that the editorial content of the sustainability report is relevant and consistent with the bank's strategy on sustainability issues;

- •transition plan: Palatine does not have its own transition plan for this first financial year.

Organization of the permanent control system

The internal control system defined by Groupe BPCE contributes to the management of risks of all kinds. It is framed by a governing charter – the Group Internal Control Charter – which stipulates that this system is designed, in particular, to ensure “[...] the reliability of financial and non-financial information reported both inside and outside the Group”.

In connection with its governing charter, BPCE has defined a permanent control system aimed at ensuring the quality of the financial and non-financial information produced, in accordance with the requirements of the order of 3 November 2014 on internal control and all other regulatory obligations relating to the quality of reports. In order to ensure strict independence in the implementation of controls, this system is based on two levels of controls. This system has been set up within Palatine.

For the publication of sustainability information; this permanent control system aims to ensure, in particular, compliance with the requirements defined by the CSRD (Corporate Sustainability Reporting Directive) and by the Group in the preparation and publication of reports and management indicators.

First-level control framework

Each unit participating in the sustainability report process implements its own formal system of self-checks and controls aimed at identifying anomalies and putting in place remediation plans to resolve them sustainably.

The director responsible for the production and publication of the sustainability report ensures that these first-level controls are carried out by all parties involved in the production process.

- •the existence of a set of documents (procedures, operating guidelines and management framework) dedicated to the production of the sustainability report, describing the production process and the first-level controls envisaged;

- •the implementation of a self-monitoring procedure and hierarchical validation of the information provided in the sustainability report;

- •the implementation of checks to ensure compliance with regulations on data to be published, including in particular:

- •reconciliations with financial statements or other reports, where applicable,

- •analysis of changes;

- •a review of data collected from suppliers (external or internal), including a check on the quality of the sources (particular attention should be paid to computer-generated and manual sources);

- •the existence of audit trails, the establishment of the indicators communicated or used in the production of the report;

- •documentation and reporting of limitations (i.e. degraded procedures for the production of certain indicators).

Level two controls: independent review of the sustainability report

A second-level control, known as the Independent Review of Reports, is implemented by a function independent of the actors in charge of producing the sustainability report, namely the Financial Control of Palatine.

The main objective of this review is to obtain reasonable assurance that the report is produced and published in a satisfactory internal control environment and that it contains reliable, clear, useful and auditable data. It takes place in 3 main phases:

- 1a phase involving the implementation of Level 2 controls, structured around 6 areas of analysis focusing on the quality of the documentation (including the double materiality analysis - DMA), the robustness of the organisation responsible for producing and publishing the report, the quality of the audit trail for the data and/or indicators included in the reporting, the effectiveness of the Level 1 control framework, the accuracy of the published data and/or indicators and their consistency with the information contained in other publications, and the clarity of the information;

- 2a feedback phase: the results of the controls are set out in a summary report detailing the work carried out and its conclusions, specifying in particular any irregularities identified and, where applicable, the recommendations made (or action plans or corrective measures), and are then submitted to the Bank’s Internal Control Coordination Committee (3CI) and Audit Committee;

- 3a monitoring phase for corrective actions (recommendations issued) and/or identified areas for improvement: the implementation of corrective actions (action plans) and/or identified areas for improvement is monitored in conjunction with the business lines and after the publication of the sustainability report in order to strengthen the system for subsequent publications. This monitoring is reported to the Bank's Coordination Committee for Internal Control (3CI) and the Audit Committee.

1.3.4.2Main features of ESG risk management

Definition of ESG risks

Environmental risks

- •physical risks arising from the impacts of extreme or chronic climate or environmental events (biodiversity, pollution, water, natural resources) on the activities of Palatine or its counterparties;

- •transition risks arising from the impacts of the transition to a low-carbon economy, or one with a lower environmental impact, on Palatine or its counterparties, including regulatory changes, technological developments, and the behaviour of stakeholders (including consumers).

Social risks

Social risks arise from the impacts of social factors on Palatine’s counterparties, including issues related to the rights, well-being and interests of individuals and stakeholders (the Company’s workforce, employees of the Company's value chain, communities concerned, end users and final consumers).

Governance risks

Governance risks arise from the impacts of governance factors on Palatine’s counterparties, including in particular issues related to ethics and corporate culture (governance structure, business integrity and transparency, etc.), supplier relationship management, influence activities and business practices.

ESG risk management framework deployment program

The ESG Risk department coordinates the implementation of the ESG risk management system at Groupe BPCE level through a dedicated program. This program is part of the Vision 2030 strategic project and defines a multi-year action plan (2024-2026) aimed at covering all regulatory requirements relating to ESG risk management. It is directly linked to the strategy and actions implemented by the Impact program. This programme is monitored quarterly by the ESG Risk Committee and by the Groupe BPCE Supervisory Board.

- •ESG risk governance: committee procedure, roles and responsibilities, remuneration;

- •strengthening knowledge of risks: monitoring systems, sector analyses and assessments, risk benchmarks, risk analysis methodologies and processes, data;

- •the operational integration of the work: in coordination with other functions within the Risk Management Department, taking ESG risk factors into account in their respective management systems and decision-making processes;

- •consolidated risk management mechanisms: dashboards, contributions to RAF/ICAAP/ILAAP systems, training and acculturation plan for board members, senior executives and employees, contribution to extra-financial communication.

In 2025, this program was subject to occasional adjustments to take into account the gradual framing of certain work and the regulatory expectations resulting from the EBA guidelines on ESG risk management.

The execution of this program mobilizes the main internal stakeholders in terms of ESG risks, in particular the impact department, the teams and functions of the other departments of the risk department, the finance department, the compliance department, the technologies and operations department, the digital & payment department as well as Groupe BPCE business lines, in particular the departments in charge of developing sustainable finance activities.

Integration of ESG risks into the risk management framework

Based on specific ESG risk assessment methodologies, Groupe BPCE is gradually integrating ESG risk factors into its operational decisions through existing systems in the bank’s main risk channels.

The climate risk identification and assessment process is described in section 1.4.1.1.2 of the ESRS 2 chapter.

Non-financial risks notably cover business continuity risks, reputational risks and legal risks. Reputational risk has been identified as material in the sections on Climate change, Own workers, Consumers and end-users, and Business conduct. These various risks are covered in the following sections:

Business continuity risks

Groupe BPCE's incident tracking and operational risk monitoring tool makes it possible to specifically identify incidents related to climate and environmental risks, thus facilitating the continuous monitoring of their number and their financial repercussions.

As a preventive measure, as part of its business continuity system, Groupe BPCE assesses the climate and environmental risks to which its main operating sites (head offices and administrative buildings) are exposed. These risks are taken into account as part of the business continuity plans defined at the level of Groupe BPCE and its entities. These define the procedures and resources to be implemented in the event of natural disasters in order to protect employees, assets and key activities and ensure the continuity of essential services.

Groupe BPCE’s essential, critical or important service providers (PECI) are also subject to an assessment of their business continuity plan, which must take into account the climate and environmental risks to which they are exposed.

Reputational risk

The management of reputational risk arising from ESG issues is fully integrated into the overall reputational risk management system described in the dedicated section of the Pillar III report.

ESG issues are the subject of particular attention in Groupe BPCE's main operational decision-making processes, such as credit granting or purchasing processes, in order to ensure compliance with its voluntary commitments (ESG sector policies in particular) and to identify controversies likely to involve the Group. Specific provisions for crisis management are also provided for.

Reputation events related to ESG issues are subject to specific monitoring at Groupe BPCE level, carried out jointly by the communication department and the ESG risk department.

Legal risks

The legal risk management framework relating to ESG issues is part of Groupe BPCE's overall legal risk management system as well as the operational risk management framework, which includes the management of litigation and reputation risks. These frameworks define the governance mechanisms and procedures for escalating identified or actual litigation risks within Groupe BPCE.

The management of litigation risks in connection with ESG issues, and in particular climate and environmental issues, is notably based on a monitoring system implemented by the Legal department on litigation affecting large corporations and in particular financial institutions. Based on this monitoring, a quantification of the risk, through the definition of fictitious standard disputes to which the Group could be exposed, is carried out and integrated into the overall quantification of Groupe BPCE's legal risk.

The risk prevention and control system is based on existing decision-making processes to limit exposure to the risk of greenwashing and the risk of non-compliance with voluntary commitments as well as failures in the exercise of the duty of care.

1.3.5GOV 4 - Statement on due diligence

The table below maps the information concerning the due diligence procedure included in Palatine's sustainability report.

Core elements of due diligence

Sections in the statement relating to sustainability

a) Embedding due diligence in governance, strategy and business model.

1.2.1.1 / 1.2.1.2 / 1.3.2

b) Engaging with affected stakeholders in all key steps of the reasonable due diligence.

1.2.2

c) Identifying and assessing adverse impacts.

1.4.1 / 2.2.2.1

d) Taking actions to address those adverse impacts.

2.2.3.1 / 2.2.3.4 / 3.2.3.3 / 3.2.3.4 / 3.4.3.3 / 3.4.3.4

e) Tracking the effectiveness of these efforts and communicating.

2.2.3.10 / 2.2.4.1 / 3.2.4.1 / 3.4.4.1

1.4Impact, risk and opportunity management

1.4.1Double materiality analysis

The double materiality exercise is the starting point for the preparation of the sustainability report.

Double materiality has two dimensions: i) materiality from an impact point of view and ii) materiality from a financial point of view.

The impacts, risks and opportunities which are identified as material represent the matters on which the content of the sustainability report is based.

1.4.1.1Methodology for identifying impacts, risks and opportunities (IRO)

1.4.1.1.1Methodology applied to all impacts, risks and opportunities (IRO)

- 1Identification of topics, sub-topics and sub-sub-topics:

- •from ESRS 1 (AR 16.) : Identification was carried out for topics, sub-topics and sub-sub-topics as defined in ESRS 1 (AR 16.). This identification was carried out by mobilising internal sources, such as the ESG matters identified in Groupe BPCE’s 2022 and 2023 NFPS reports and the 2024 sustainability report, the reasonable due diligence process put in place by the Group as part of the duty of care plan and the existing risks mapping, supplemented by external sources, such as the analysis of a business sector benchmark, with a focus on the most relevant matters for banking players;

- •entity-specific: moreover, the analysis conducted by Groupe BPCE is not limited to the sub-sub-topics of ESRS 1 (AR 16.) ; the use of internal and external sources also leads to the identification of issues specific to the Group's banking and insurance activities. The following items have been identified as specific to Groupe BPCE and the resulting material IROs are included in the list of IROs (refer to Section 1.4.2 List of material IROs):

- −ESRS S1: the specific sub-topic: Attractiveness, employee loyalty and engagement (including the specific sub-sub-topics: Listening to employees and strengthening their commitment, Integration of new recruits and employee loyalty, Recruitment strategy and employer brand);

- −ESRS G1: the specific sub-topic: Fight against money laundering and the financing of terrorism and compliance with sanctions measures (national, European or international), embargoes and asset freezes;

- In 2025, the relevance of the list of the Group's topics, sub-topics and sub-sub-topics was questioned. In view of the Group's benchmark and challenges, this list has not changed.

- 2Formulation of Impacts, Risks and Opportunities (IRO): work to identify the IRO within each topic was carried out in order to cover both impact materiality and financial materiality. Several internal and external sources were used to identify IROs. For the purposes of double materiality analysis, risks and opportunities generally arise from a positive or negative impact, or from the Group's dependence on resources and people.

- 3Relevance of the IRO: the relevance of each IRO was verified with the business lines concerned to ensure that the listed IRO effectively reflected a Risk, Opportunity or Impact for Groupe BPCE, to qualify the Impacts as positive or negative for the same sub-topic and to avoid duplication between similar IRO. In 2025, the relevance of the IRO identified in 2024 was reviewed and work was carried out to group the IROs together to avoid the same subject being dealt with by several IRO of the same type.

- 4Characteristics of the IRO: for each IRO identified, a rating was prequalified. This prequalification consisted of:

- - positioning each IRO in Groupe BPCE’s value chain, i.e. upstream, within its own activities, or downstream;

- - defining the potential or actual nature of the negative and positive impacts.

Consideration of the value chain in the identification of Palatine's IROs

The activities of Palatine and its entire upstream and downstream value chain were taken into account in the double materiality analysis. The following guidelines were adopted in view of the specific nature of Palatine's business segment:

- •Mapping its activities and the players in the value chain to identify which players are in risk areas;

- •Carrying out an analysis by major families of players: customers, suppliers, subcontractors, etc.;

- •extending this analysis beyond first-level and direct business relationships: the business lines took into consideration, in addition to the major families of direct stakeholders in the value chain, the entire environment surrounding them, in particular through sectors analysis.